Structured settlements provide long-term financial security for many individuals who have won lawsuits or received personal injury settlements. Instead of receiving a lump sum, recipients are paid periodic installments over time, which can help ensure a steady income. However, life is unpredictable, and sometimes you may need quick cash to cover emergencies, pay off debts, or invest in opportunities that can’t wait.

This article explores the options available for getting fast cash from a structured settlement, the pros and cons, and important considerations to make informed decisions.

1. Understanding Structured Settlements

Before exploring how to access quick cash, it’s essential to understand what a structured settlement is:

a. Definition

A structured settlement is a financial arrangement where a plaintiff in a lawsuit receives compensation over a set period rather than as a single lump sum. Payments may occur weekly, monthly, or annually.

b. Purpose

- Provide long-term financial security

- Protect recipients from spending large sums too quickly

- Ensure ongoing support for medical or living expenses

c. Typical Scenarios

- Personal injury settlements

- Workers’ compensation cases

- Wrongful death settlements

- Other legal claims requiring financial restitution

Structured settlements are designed to last for years, often decades, providing peace of mind to recipients.

2. Why You Might Need Quick Cash

Even with a structured settlement, emergencies and financial opportunities can arise that require immediate funds. Common reasons include:

- Medical emergencies: Unplanned procedures or treatments not fully covered by insurance

- Debt repayment: Credit card balances, mortgages, or personal loans

- Investment opportunities: Business ventures, real estate deals, or education

- Lifestyle changes: Home repairs, relocation, or family needs

While structured settlements provide stability, they may not always meet urgent, large cash demands.

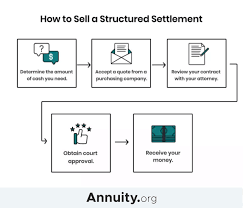

3. Options for Accessing Quick Cash

a. Selling Your Structured Settlement (Structured Settlement Factoring)

One of the most common ways to access quick cash is by selling part or all of your future payments to a structured settlement company. This process is called factoring.

How it works:

- Receive an offer from a settlement buyer. They will evaluate your settlement and propose a lump sum.

- Court approval is usually required to ensure the sale is in your best interest.

- Receive cash after approval, typically within weeks.

Pros:

- Immediate access to cash

- Can cover emergencies or high-priority expenses

- Flexible amounts depending on the company and agreement

Cons:

- Lump sum is usually less than the total future payments

- Some companies charge fees and service costs

- Court approval can take time

b. Structured Settlement Loans

Some financial institutions offer loans secured against future settlement payments. These are different from selling because you retain the settlement but use future payments as collateral.

Pros:

- You retain long-term settlement benefits

- May have lower costs than factoring

Cons:

- Interest rates can be high

- Defaulting may risk losing future payments

c. Borrowing from Family or Friends

While not formal financial advice, some recipients turn to trusted family or friends for short-term loans secured against future settlement income.

Pros:

- No high-interest rates or fees

- Flexible repayment terms

Cons:

- Can strain personal relationships

- May not provide large sums

d. Using Savings or Retirement Accounts

If you have other assets, such as emergency savings or retirement accounts, tapping them may be an option. This avoids factoring fees but can have tax implications or penalties.

4. How Structured Settlement Factoring Works

Structured settlement factoring is the most common method for getting quick cash. Here’s a detailed step-by-step process:

- Evaluate your needs – Determine exactly how much cash you require.

- Research companies – Not all companies offer fair terms. Look for licensed, reputable firms.

- Get multiple quotes – Compare offers to ensure the best lump sum for your settlement.

- Submit documentation – Provide settlement papers, identification, and sometimes proof of expenses.

- Court review and approval – Courts review the deal to confirm it’s in your best interest and that the company complies with legal requirements.

- Receive funds – Once approved, funds are typically disbursed quickly, often in days or weeks.

5. Benefits of Getting Quick Cash

- Immediate financial relief: Cover urgent expenses without waiting for installment payments.

- Debt management: Pay down high-interest debts quickly.

- Flexibility: Use the cash for personal, medical, or investment needs.

- Peace of mind: Reduce stress associated with urgent financial situations.

6. Risks and Considerations

While structured settlement factoring can provide quick cash, it’s important to weigh potential risks:

- Loss of long-term income: Selling future payments reduces guaranteed income.

- Fees and discount rates: Settlement buyers usually purchase payments at a discount, meaning you receive less than the total future value.

- Scams: Some unlicensed companies may exploit recipients. Always verify licensing and reputation.

- Tax implications: Generally, structured settlements are tax-free, but certain transactions may have tax consequences if not handled properly.

7. Tips for Choosing a Factoring Company

- Check licensing: Verify the company is licensed in your state.

- Compare offers: Don’t accept the first quote. Multiple offers ensure you get fair value.

- Read reviews: Look for complaints or customer experiences online.

- Understand fees and discounts: Ask for the exact amount you’ll receive and the total value of your future payments.

- Consult a financial advisor or attorney: Professional guidance helps protect your long-term financial interests.

8. Legal and Court Requirements

Structured settlements are protected by law. Selling or borrowing against payments usually requires court approval:

- Why court approval is necessary: To ensure the transaction is in your best interest and not exploitative.

- Process: Submit the agreement, show the need for cash, and wait for judicial review.

- Timeline: Court approval can take weeks but ensures the sale is legal and binding.

9. Case Studies

Case Study 1: Emergency Medical Expenses

Lisa, a settlement recipient, needed $20,000 for urgent medical treatment. She sold a portion of her monthly payments to a licensed factoring company. After court approval, she received funds within 10 days, covering her bills without financial strain.

Case Study 2: Investment Opportunity

David wanted to invest in a business opportunity but lacked liquid cash. He sold part of his structured settlement, received a lump sum, and successfully invested in a business that grew his wealth.

These examples show how factoring can be strategic when urgent or important needs arise.

10. Alternatives to Factoring

If selling your settlement doesn’t feel right, consider alternatives:

- Structured settlement loans: Retain future payments but borrow against them.

- Emergency savings: Use personal funds to avoid selling.

- Debt restructuring: Refinance high-interest debt to reduce immediate pressure.

- Crowdfunding or community support: Rare but sometimes effective in emergencies.

11. Questions to Ask Before Selling

- How much will I actually receive after fees?

- What portion of my future payments will I sell?

- How long will the court approval process take?

- Is the company licensed and reputable?

- Are there alternatives that allow me to keep more of my settlement intact?

Asking these questions helps protect your financial future.

12. Conclusion

Getting quick cash from a structured settlement can be a practical solution for emergencies, debt, or investment opportunities. The most common method is structured settlement factoring, which allows you to sell part or all of your future payments for immediate funds. However, it’s important to consider long-term impacts, legal requirements, and fees before proceeding.

Consulting with financial advisors and licensed factoring companies ensures that you make informed decisions while protecting your financial security. Structured settlements are designed to provide stability, but with careful planning, they can also offer the flexibility to meet urgent financial needs.

By understanding your options, evaluating risks, and acting strategically, you can access cash when needed without jeopardizing your future income.

Summary:

A structured settlement is a financial or insurance arrangement, including periodic payments, that a claimant accepts to resolve a personal injury tort claim or to compromise a statutory periodic payment obligation.

Keywords:

Cash for your structured settlement, structured settlements, Structured Settlement

Article Body:

Just because you received a structured settlement for your lawsuit, it doesn’t mean you have to wait for years to get the money. There are many settlement purchasing companies that will give you instant cash for your structured settlement. These companies can pay cash for the entire structured settlement or purchase your remaining periodic settlement payments. You can spend this lump-sum payment on anything-a house, college tuition, business investments or debts.

What Is a Structured Settlement?

A structured settlement, which typically results from a personal injury lawsuit, is an agreement where you consent to accept payments over time in exchange for the release of liability for your claim. A structured settlement can provide payments in almost any manner you choose. For example, the settlement may be paid in annual installments over a number of years or in periodic payouts every few years.

These payments are generally awarded through the purchase of one or more annuities from a life insurance company. Structured settlements can also be used with lottery winnings, contest prize money and other situations with substantial cash awards.

Structured Settlements Not Always the Best Fit

In theory, structured settlements are designed to provide long-term financial security to injury victims through tax-free payments. And for most people, the agreed-upon structured payment plan initially makes sense. However, a financial emergency, a business opportunity, an unforeseen medical expense, or a house purchase can put a strain on the injured party’s finances.

And the structured nature of the settlement may become too restrictive to cover major financial purchases. Also, a structured settlement may not be the best option for investing. There are many other investment vehicles that can generate greater long-term return than the annuities used in structured settlements. Therefore, some people may be better off getting cash for their structured settlement and then building their own investment portfolio.

How Getting Cash for a Structured Settlement Works

If you receive an award from your injury case, an attorney or financial advisor will likely recommend setting up periodic installment payments instead of giving you a lump sum of cash up front for your structured settlement. Then, an independent third party will purchase an annuity that will provide you with tax-free periodic payments.

Companies that offer cash for structured settlements have a variety of programs that can allow you to access any portion of your annuity. For example, you may want to sell as little as four year’s worth of payments or receive a lump-sum payment while still enjoying some portion of your monthly payment. Or you can sell your settlement for a large payment that is five or six years in the future. You can also customize an arrangement to get cash for a structured settlement based on your unique needs.

Here’s an example of how obtaining cash for a structured settlement works: Let’s say you were in an accident five years ago. The accident caused you to be hospitalized for several months and undergo nearly a year’s worth of physical therapy. So you hired an attorney and sued the responsible individual-or, rather, the person’s insurance company. Ultimately, your attorney advises you that you’ll be awarded a substantial sum of money.

After several months or years of negotiation, you receive a sizable settlement. However, the cash you get upfront is only enough to cover the medical expenses. The rest of your compensation is scheduled to be paid out in regular installments through an annuity over the next 15 to 30 years. Rather than being restricted to monthly or annual payments, you contact a settlement purchaser to secure immediate cash for your structured settlement. You’re then able to use the cash to enhance your current cash flow-rather than waiting on periodic future payments.

Legal Issues of Receiving Cash for a Structured Settlement

If you’re contemplating getting cash for your structured settlement, it’s important to contact a financial advisor. Most states have regulations that limit the sale of structured settlements, so you’ll need court approval to receive cash for your structured settlement. Federal restrictions also may affect the sale of structured settlements to a third-party individual. And some insurance companies won’t transfer annuities to third parties.

Also, before you attempt to obtain cash for a structured settlement, be sure to do your homework. Check out multiple companies to see which one can offer you the most cash for your structured settlement. You also want to examine their integrity, reputation and track record. This will help ensure you have the most positive experience obtaining cash for your structured settlement.

Receiving cash for a structured settlement is an ideal option if you need a lump sum of money to meet your immediate needs.

Tinggalkan Balasan