Introduction

Debt is one of the most common financial challenges faced by individuals and businesses alike. While debt can be a useful tool when managed strategically, unmanaged or excessive debt often becomes a barrier to growth, freedom, and long-term stability.

In today’s economic environment—marked by rising costs, interest rate fluctuations, and financial uncertainty—getting out of debt is no longer just a personal finance goal. It is a leadership decision, a strategic reset, and a commitment to sustainable financial health.

This article provides a CEO-friendly, professional, and practical guide to getting out of debt. It avoids emotional language and quick-fix promises, focusing instead on structured thinking, clear priorities, and disciplined execution. Whether you are an individual professional, entrepreneur, or decision-maker, the principles outlined here are designed to help you regain control and build a stronger financial foundation.

Understanding Debt from a Strategic Perspective

Debt Is Not Always the Enemy

From a leadership standpoint, debt itself is not inherently negative. In fact, debt is often used to:

- Finance education or skill development

- Build businesses

- Acquire assets

- Smooth cash flow

The problem arises when debt no longer serves a strategic purpose and instead limits flexibility, increases stress, and erodes long-term value.

Effective leaders do not ask, “Do I have debt?”

They ask, “Is this debt working for me or against me?”

The Difference Between Productive and Unproductive Debt

Productive debt typically:

- Generates future income

- Increases earning potential

- Has manageable interest rates

- Fits within a clear repayment plan

Unproductive debt often:

- Funds consumption rather than growth

- Carries high interest rates

- Grows faster than income

- Creates long-term dependency

Getting out of debt begins with recognizing which category your debt falls into.

Why Getting Out of Debt Matters

Financial Freedom and Decision Power

Debt reduces optionality. When large portions of income are committed to repayments, choices become limited.

Reducing or eliminating debt:

- Increases cash flow

- Improves resilience during uncertainty

- Expands personal and professional opportunities

Freedom is not about having unlimited money—it is about having control.

Mental Clarity and Leadership Performance

Chronic financial stress affects decision-making quality. Leaders under pressure are more likely to:

- Make short-term decisions

- Avoid calculated risks

- Experience burnout

A healthier financial position supports clearer thinking, better leadership, and long-term focus.

Long-Term Wealth Creation

Interest works in two directions. When you owe money, interest works against you. When you invest, interest works for you.

Getting out of debt is often the first step toward:

- Building investments

- Creating emergency reserves

- Achieving financial independence

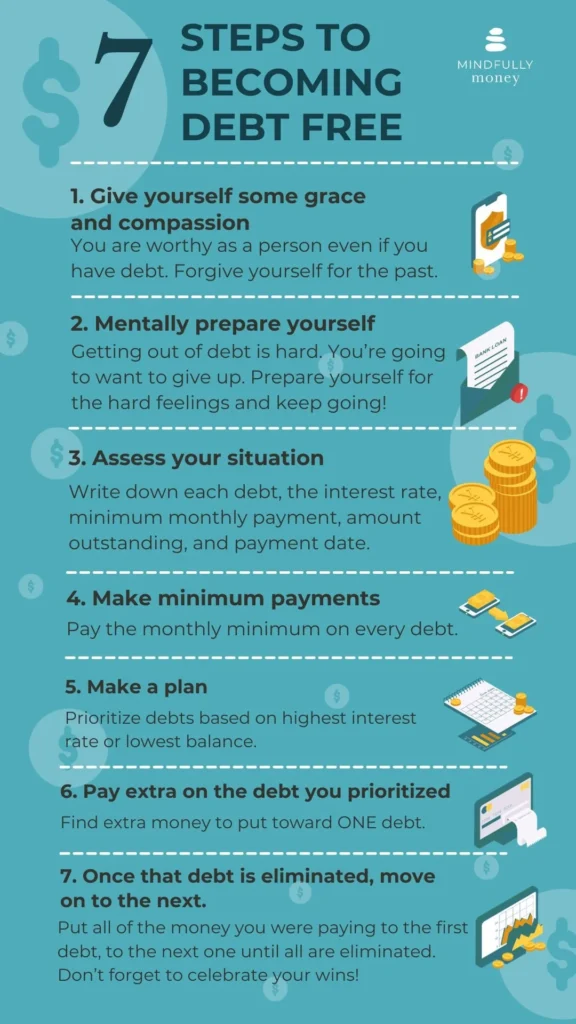

Step One: Assess the Full Picture

Conduct a Financial Audit

Strong decisions start with accurate information. Begin by listing:

- All debts

- Interest rates

- Minimum payments

- Remaining balances

- Payment due dates

Avoid judgment. This step is about clarity, not blame.

Understand Cash Flow

Next, analyze income and expenses:

- Fixed expenses

- Variable spending

- Discretionary costs

Debt repayment capacity depends on cash flow discipline, not income alone.

Step Two: Define Clear Objectives

Set a Strategic Goal

“Getting out of debt” is too vague. Effective goals are:

- Specific

- Measurable

- Time-bound

For example:

- Eliminate high-interest debt within 18 months

- Reduce total debt by 40% in two years

- Become consumer-debt-free before a major life milestone

Clear goals create accountability.

Align Goals with Life Priorities

Debt reduction should support—not undermine—your broader objectives, such as:

- Career growth

- Family stability

- Business development

- Health and well-being

Strategy fails when financial goals ignore human realities.

Step Three: Choose a Debt Reduction Strategy

The Snowball Approach

This method prioritizes paying off the smallest balances first.

Advantages:

- Quick wins

- Psychological momentum

- Increased motivation

Best for individuals who value behavioral reinforcement.

The Avalanche Approach

This strategy focuses on debts with the highest interest rates first.

Advantages:

- Minimizes total interest paid

- Faster financial efficiency

- Mathematically optimal

Best for those comfortable with longer timelines before visible progress.

A Hybrid Strategy

Many leaders adopt a blended approach:

- Eliminate one small balance for momentum

- Then shift focus to high-interest debt

The best strategy is the one you will execute consistently.

Step Four: Optimize Spending Without Sacrificing Stability

Reduce Expenses Strategically

Cutting costs does not mean sacrificing quality of life. It means:

- Eliminating inefficiencies

- Reducing low-value spending

- Redirecting resources intentionally

Ask:

“Does this expense align with my priorities?”

Avoid Extreme Deprivation

Unsustainable budgets fail. Overly aggressive cuts often lead to burnout and reversal.

Effective cost control is:

- Realistic

- Repeatable

- Aligned with long-term habits

Step Five: Increase Income Intentionally

Leverage Existing Skills

Debt reduction accelerates with higher income. Consider:

- Negotiating compensation

- Taking on consulting or freelance work

- Monetizing specialized skills

Focus on high-impact income, not endless hustle.

Avoid Lifestyle Inflation

As income increases, resist expanding expenses. Redirect additional income toward:

- Debt repayment

- Emergency savings

- Long-term investments

This discipline shortens the debt timeline significantly.

The Role of Emergency Savings

Why an Emergency Fund Matters

Without a financial buffer, unexpected expenses often lead to new debt.

An emergency fund:

- Prevents regression

- Reduces stress

- Protects progress

Even a modest reserve can make a significant difference.

Build While Paying Down Debt

Contrary to common belief, small emergency savings can coexist with debt repayment. The goal is risk reduction, not perfection.

Avoiding Common Debt Traps

Relying on Consolidation Without Behavior Change

Debt consolidation can simplify payments, but it does not solve spending habits.

Without discipline:

- Old debt returns

- New debt accumulates

- Progress stalls

Tools do not replace behavior.

Emotional Spending

Stress, boredom, and social pressure often drive unnecessary spending.

Leaders manage emotions as carefully as finances. Awareness is a powerful defense.

Ignoring Long-Term Planning

Debt elimination is not the end goal—it is the foundation.

Without a post-debt plan, financial drift returns.

The CEO Mindset Applied to Personal Debt

Think Like a Business

Strong organizations:

- Track performance

- Manage liabilities

- Invest strategically

- Plan for risk

Apply the same principles to personal finance.

Measure Progress Regularly

Set review intervals:

- Monthly payment reviews

- Quarterly net-worth assessments

- Annual financial planning

Visibility drives accountability.

Celebrate Milestones

Progress deserves recognition. Strategic rewards reinforce discipline and motivation.

When Professional Help Makes Sense

Financial Advisors and Credit Counselors

In complex situations, professional guidance can:

- Improve strategy

- Reduce mistakes

- Offer objective perspective

Choose advisors who educate, not pressure.

Legal and Credit Considerations

For severe debt cases, structured solutions may exist. These should be explored cautiously and as part of a long-term recovery plan.

Life After Debt: What Comes Next

Redirect Cash Flow

Once debt is reduced or eliminated:

- Build investments

- Strengthen savings

- Support personal growth goals

Debt freedom increases optionality.

Build Long-Term Wealth

Without debt pressure, compounding works in your favor. Time becomes an ally instead of a threat.

Maintain Financial Discipline

Debt-free status requires ongoing discipline. Sustainable habits matter more than past success.

Conclusion

Getting out of debt is not about restriction—it is about reclaiming control. It is a strategic decision that enhances freedom, resilience, and long-term opportunity.

Approached with a CEO mindset, debt reduction becomes:

- Structured

- Intentional

- Achievable

The goal is not perfection, but progress. With clarity, discipline, and patience, financial stability becomes a natural outcome—not a distant dream.

True leadership starts with ownership—of decisions, priorities, and the future.

Summary:

Getting Out of Debt, The Smart Credit-Card Plan, the perfect paydown strategy

Behavioral economist Meir Statman, recently said �getting out of debt is the financial equivalent of trying to quit smoking.” Just like any bad habit, good intentions alone will not be enough. To ensure success, we need to break our underlying patterns of behavior. How is it we live in the richest most powerful country in the world, but the average American is more than $11,000 in debt. Our Europ…

Keywords:

Article Body:

Getting Out of Debt, The Smart Credit-Card Plan, the perfect paydown strategy

Behavioral economist Meir Statman, recently said �getting out of debt is the financial equivalent of trying to quit smoking.” Just like any bad habit, good intentions alone will not be enough. To ensure success, we need to break our underlying patterns of behavior. How is it we live in the richest most powerful country in the world, but the average American is more than $11,000 in debt. Our European friends who live by a mainly debit card system have an average savings of $13,000. On a recent visit to Germany, I was shocked to find that less than 35% of all the shops and restaurants accepted credit cards. What would we need to do to reverse this trend and get into a (plus) situation.

Plastic Surgery

If we are serious about paying off our balances. We don’t have to literally cut up our credit cards, just stop using them routinely. We should go green for our everyday spending. Try carrying around a set amount of cash to use each week. We make better purchasing decisions when we actually have to hand over the green stuff plus there’s a preset spending limit. When we run out of money, we stop spending it’s that simple. When the only way to purchase is plastic, buying online for instance, then use your debit card. Your debit card can also be used as an emergency substitute for cash should you run out.

Leave Those Cards At Home

The best way to ensure that you enforce the cooling off period on new credit purchases is by taking the cards out of your wallet. You should store them in a place that’s not easily accessible and safe. Do not let others know where you have hidden them.

Close The Accounts No Longer Needed

Having unused credit available from lenders with whom you’ve had a long relationship will help boost your credit score. Having too many will harm your credit score. As a rule, 3 credit cards is what works best and try to never spend more than 50% of the available credit on any of the cards. This will keep your score at it’s highest. You should also consider closing all your store cards, if you need to make a purchase then use your credit card and pay it off at the end of the month.

Lowering Your Interest Rates

Start by reducing what you pay in interest. We can start by calling our current credit card companies and explaining that we intend to transfer our balance to another issuer unless our interest rate is lowered. Almost all credit card companies run promotional programs with low or 0% interest. They will be willing to put you on one of those rather than risk losing your business. All you need to do is ASK.

Tackling Those Credit Card Balances

Finally we need to develop a strategy for paying off our existing credit card balances.

Gather all your credit card statements together and make a simple table listing the entire amount you owe, and the minimum payment and interest rate for each card. This will help us determine the order in which we should pay off our cards. We need to focus on the highest interest rate cards first and pay off as much as you can each month while making only the minimum payments on our other cards. When the first card is paid off, use the same strategy on the next-highest interest rate card and so on until you’re debt-free.

Late Payments

Are the number one cardinal sin of debt management. You get hit with hefty late fees and very high penalty rates that can go to 30%, plus of course your credit score will take a big hit.

We all have a responsibility to improve our financial literacy and develop the required skills and practices for effective financial management. There is a real need to get away from the �Someday things will get better in my life� or the �Someday I will be able to earn enough money to stop worrying about the bills. There is a lot more to life than that, but it has to be said and understood that the only person that can change your life is YOU. There is NO substitute for Action! With Action, you will overcome your fears and hesitations and accomplish everything you set out to do and more.

Have an opinion or a question you would like me to answer, then write me! http://www.CarlHampton.com

Tinggalkan Balasan